Key points:

- Lockheed Martin (LMT) relies on U.S. and foreign governments for roughly 93% of its revenues.

- While LMT recorded flat Y/Y revenue growth in Q1 2026, the company is sticking to its ~5% revenue growth target for 2026. This aspiration is supported by a 7.7% Y/Y increase in LMT’s backlog.

- LMT expects its operating margin to improve in the remainder of 2026, supporting a sizable increase in earnings per share, with EPS seen at around $30/share for the full year.

- To achieve its growth ambitions, LMT is significantly increasing its capital expenditures, resulting in a circa 4% decrease in free cash flow for the year.

- With revenue growth trailing backlog growth since 2022, LMT’s topline momentum will likely continue in 2027. TenderAlpha’s government and supply chain data allow investors to track LMT’s contracting activity in real time via recently launched TenderAlpha Pro.

Lockheed Martin’s Major Customers and Trade Flows Counterparties

Before examining Lockheed Martin’s latest financials, let’s first go through the company’s key government customers and B2B trade flows relationships, which will allow us to get a better idea of the main driving factors behind LMT’s financial performance.

Activity as a government supplier

While LMT’s overall government award transactions count peaked in 2022 at marginally above 35,000, recent inflation and persistent awards of high-value government contracts have resulted in a steady rise in the overall value of LMT’s government contract awards, reaching almost $74 billion in 2025, or an annual increase of 21% since 2021, as per TenderAlpha government contracts data:

Table 1: Lockheed Martin government contracting activity, 2021–2026

| Year | Total Value (USD) | Number of Federal Contract Transactions |

|---|---|---|

| 2026 | 12,305,887,229 | 5,933 |

| 2025 | 73,777,669,134 | 31,009 |

| 2024 | 50,994,700,645 | 33,049 |

| 2023 | 70,857,714,969 | 34,167 |

| 2022 | 45,643,598,942 | 35,092 |

| 2021 | 33,984,168,559 | 30,358 |

With approximately 93% of all 2025 LMT revenue coming from government entities (72% from the U.S. government alone and 21% from foreign military sales), public procurement remains a pillar of LMT’s topline. Among major direct customers we see the Department of the Navy, the Department of Defense, and the Department of the Air Force. Contracts awarded by specific DoD components, such as the Department of the Navy, are counted separately from contracts listed directly under the Department of Defense. As a result, the figures should be read by the contracting entity and should not be added together as a single DoD total.

Table 2: Top five Lockheed Martin government customers, 2010–2026

| Contracting Entity | Value of Contracts (USD) | Number of Federal Contract Transactions |

|---|---|---|

| Department of the Navy | 246,171,845,057 | 12,288 |

| Department of Defense | 141,463,409,097 | 297,672 |

| Department of The Air Force | 116,016,474,567 | 6,554 |

| Department of the Army | 105,948,886,118 | 3,839 |

| Missile Defense Agency | 18,562,891,949 | 132 |

To better understand Lockheed Martin’s broader defense-industrial ecosystem, TenderAlpha’s global trade flows data identifies major counterparties associated with inbound and outbound shipment activity involving the company. Because these records may reflect supplier, subcontractor, partner, logistics, research, or program-related activity, they are best read as indicators of relationship intensity rather than direct measures of procurement spend or recognized revenue.

Table 3: Key B2B counterparties associated with Lockheed Martin trade flows, 2019–2026

| Counterparty | Trade flows profile | Inbound flow | Outbound flow |

|---|---|---|---|

| Northrop Grumman | Inbound and outbound activity | High | High |

| Boeing | Inbound and outbound activity | High | Moderate |

| L3Harris | Primarily inbound activity | High | — |

| BAE Systems | Primarily inbound activity | High | — |

| RTX | Primarily inbound activity | High | — |

| Textron | Primarily outbound activity | — | Moderate |

| California Institute of Technology | Primarily outbound activity | — | Moderate |

| Georgia Tech Applied Research Corporation | Primarily outbound activity | — | Moderate |

The table summarizes relationship intensity across Lockheed Martin’s B2B trade flows network. Specific shipment values and shipment counts underlying these relationships are available on TenderAlpha Pro. For investors, these links may be useful as a starting point for identifying counterparties that could be exposed to changes in Lockheed’s production, program activity, and broader defense-industrial demand.

Lockheed Martin’s Financial Performance

Now that we have seen Lockheed Martin’s government contracting activity and key B2B trade-flow relationships, let’s discuss the company’s latest financial developments.

Q1 2026 Financial Results Overview

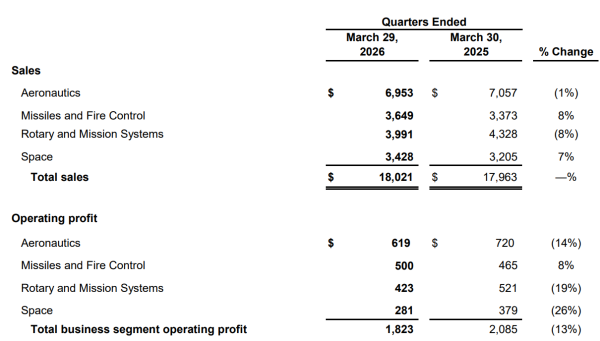

Lockheed Martin reports results in four key segments, namely Aeronautics at 39% of Q1 2026 net sales, Missiles and Fire Control at 20%, Rotary and Mission Systems at 22%, and Space at 19% of Q1 2026 net sales:

Table 4: Sales breakdown between segments

Source: Lockheed Martin Q1 2026 Financials Table

From the snippet above, we see that LMT’s Q1 2026 sales were flat Y/Y, with strength in the Missiles and Fire Control and Space segments offsetting weakness in the largest Aeronautics segment. The lack of topline growth, coupled with unfavorable profit adjustments, resulted in a 13% Y/Y slump in operating profit, pushing down LMT’s operating margin to 10.1%, 1.5% lower than the prior year quarter.

The net result for LMT was EPS of $6.44/share, a 11.5% Y/Y decline.

All in all, if we look at Q1 2026 financials alone, LMT’s momentum does not seem particularly impressive, with flat sales, lower margins, and a slump in earnings per share. As we will discuss in the remainder of the article however, things should look up for LMT later this year.

Backlog Evolution

Backlog developments were indeed more favorable, with LMT’s total backlog standing at $186.4 billion at the end of Q1 2026, up 7.7% Y/Y, most notably driven by increases in the Missiles and Fire Control, Rotary and Mission Systems, and Space segments, while Aeronautics backlog continued to decline:

Table 5: Lockheed Martin sales and backlog year-over-year evolution, 2019–2026

| Period\Indicator | Sales growth | Backlog growth |

|---|---|---|

| Q1 2026 | 0% | 7.7% |

| 2025 | 5.6% | 10% |

| 2024 | 5.1% | 9.6% |

| 2023 | 2.4% | 7% |

| 2022 | -1.6% | 10.8% |

| 2021 | 2.5% | -8% |

| 2020 | 9.3% | 2.2% |

| 2019 | 11.3% | 10.4% |

Source: Lockheed Martin Investor Materials

Given the more encouraging backlog developments, it is no surprise that LMT remains optimistic for the rest of 2026, as we will highlight in the next section.

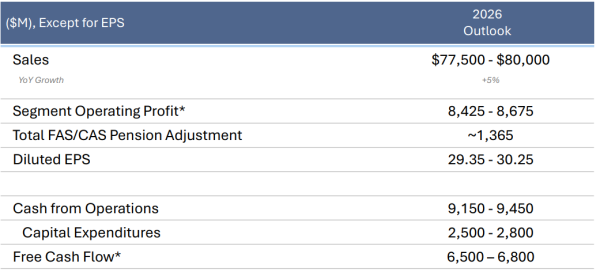

2026 Outlook

Looking ahead to the remainder of 2026, LMT is hopeful that revenue growth will pick up, reaching approximately 5% for the full year. This, in turn, should allow for a sizable increase in segment operating profit (almost 27% at the midpoint), thus pushing up EPS close to $30/share:

Table 6: Lockheed Martin 2026 Outlook

Source: Lockheed Martin Q1 2026 Results Presentation

If LMT manages to reach its 2026 outlook, the EPS increase relative to 2025 will be quite impressive at almost 40% Y/Y, although it is more reflective of a recovery from weak operating performance in 2024–2025. As a reminder, after reaching EPS of $27.55/share in 2023, LMT’s EPS has slumped in recent years, impacted by weak operating margins even as revenue growth has been quite steady throughout the period. CFO Evan Scott is confident the turnaround is gaining momentum, as discussed on the conference call:

“It is also important to note that we expect margins to improve over the course of the year with gains anticipated in the second half of 2026, as production milestones are achieved and risks are retired. We remain focused on disciplined operational execution, scaling production and delivering at speed to meet the urgency of this moment.”

The only relative financial disappointment with regard to the rest of 2026 is that LMT will have to dramatically increase its capex, ultimately resulting in a small, circa 4% decrease in free cash flow.

Conclusion

Lockheed Martin relies on U.S. and foreign governments for approximately 93% of its revenue. This makes TenderAlpha’s government contracting data particularly useful when assessing the future revenue trajectory of LMT.

With backlog growth outpacing sales growth since 2022, higher capex may help Lockheed convert demand into revenue, although execution, supply-chain performance, and program timing remain key risks.

The net result for LMT shareholders could be an EPS of around $30/share, topping the result achieved in 2023 and marking a recovery from weak operating performance in 2024–2025.

To learn more about Lockheed Martin’s G2B and B2B activity, contact us for relevant government contracting and trade flows insights.