Key points:

- Boeing (BA) derived approximately 38% of its 2025 revenue from government sources, with the significance of government buyers likely to diminish as the company works through its sizable Commercial Airplanes backlog.

- While BA’s government award transaction count peaked in 2023, the value of its government contract awards reached almost $32 billion in 2025, representing an annual increase of 12% since 2021.

- Starting in 2022, cumulative backlog growth has notably exceeded topline sales growth, supporting stronger medium-term revenue visibility, although conversion depends on execution and delivery timing.

Boeing’s Major Customers and Trade Flows Counterparties

Before examining Boeing’s latest financials, let’s first go through the company’s key government customers and B2B trade flows relationships, which will allow us to get a better idea of the main driving factors behind BA’s financial performance.

Activity as a government supplier

While BA’s overall government award transactions count peaked in 2023 at marginally below 20,000, recent inflation and persistent awards of high-value government contracts have resulted in a steady rise in the overall value of BA’s government contract awards, reaching almost $32 billion in 2025, or an annual increase of 12% since 2021, as per TenderAlpha government contracts data:

Table 1: Boeing government contracting activity, 2021–2026

| Year | Total Value (USD) | Number of Federal Contract Transactions |

|---|---|---|

| 2026 | 10,403,910,896 | 4,153 |

| 2025 | 31,801,503,207 | 17,812 |

| 2024 | 25,469,135,680 | 18,863 |

| 2023 | 24,011,454,644 | 19,604 |

| 2022 | 18,546,128,114 | 17,503 |

| 2021 | 20,132,861,014 | 14,672 |

As such, despite increased reliance on non-government revenue sources in recent years, a result of commercial aircraft demand recovery post COVID-19, U.S. and international government entities still accounted for at least 35% of Boeing’s topline in 2025, with an exact figure somewhat hard to arrive at due to insufficient disclosure in BA’s annual report. TenderAlpha Pro indicates a circa 38% exposure to government customers.

Among major direct customers we see the Department of Defense, the Department of the Air Force, and the Department of the Navy. Contracts awarded by specific DoD components, such as the Department of the Navy, are counted separately from contracts listed directly under the Department of Defense. As a result, the figures should be read by the contracting entity and should not be added together as a single DoD total.

Table 2: Top ten Boeing government customers, 2010–2026

| Contracting Entity | Value of Contracts (USD) | Number of Federal Contract Transactions |

|---|---|---|

| Department of Defense (US) | 114,816,818,261 | 24,764 |

| Department of the Air Force | 102,418,321,856 | 4,002 |

| Department of the Navy | 74,387,548,268 | 12,279 |

| Department of the Army | 25,405,685,011 | 1,737 |

| Department of Defence (Australia) | 14,091,089,106 | 3,405 |

| Defense Logistics Agency | 6,898,178,078 | 131,266 |

| National Aeronautics and Space Administration | 5,593,429,156 | 696 |

| Missile Defense Agency | 5,449,748,378 | 19 |

| U.S. Special Operations Command | 4,258,647,770 | 271 |

| Defense Advanced Research Projects Agency | 1,505,689,553 | 86 |

From Table 2 above, we see that among Boeing’s top ten government customers, there is only one non-U.S. institution, namely the Australian Department of Defence. That said, BA has been active with government contracts throughout the world, completing government projects in countries such as Afghanistan, India, New Zealand, Kuwait, and Japan, although this is typically done via U.S. foreign military sales (FMS), rather than direct local-government procurement.

Indeed, direct U.S. government procurement, including U.S. foreign military sales, accounts for the aforementioned 35% of BA’s topline coming from government revenue sources, as disclosed in the 2025 annual report. Of course, Boeing also does business with foreign governments outside the scope of U.S. foreign military sales, with individual international contracts available on TenderAlpha Pro.

B2B Activity

This context behind Boeing’s government business is important when we discuss the company’s B2B relationship with peers such as RTX and Northrop Grumman. Looking through the data on TenderAlpha Pro, we see that RTX appears to act as a recurring subcontractor and mission-systems supplier to Boeing on several Boeing-led federal and FMS defense aircraft programs.

As such, while there is intense competition among Boeing, Lockheed Martin, RTX, and Northrop Grumman for each government contract, these companies also act as subcontractors for one another, thus forming a broader defense-industrial ecosystem.

To better understand Boeing’s broader defense-industrial ecosystem, TenderAlpha’s global trade flows data identifies major counterparties associated with inbound and outbound shipment activity involving the company. Because these records may reflect supplier, subcontractor, partner, logistics, research, or program-related activity, they are best read as indicators of relationship intensity rather than direct measures of procurement spend or recognized revenue.

Table 3: Key B2B counterparties associated with Boeing trade flows, 2019–2026

| Counterparty | Trade flows profile | Inbound flow | Outbound flow |

|---|---|---|---|

| RTX Corporation | Inbound and outbound activity | High | High |

| Northrop Grumman | Inbound and outbound activity | High | Moderate |

| Lockheed Martin | Primarily outbound activity | Low | High |

| BAE Systems | Primarily inbound activity | High | — |

| Air India | Primarily outbound activity | — | Moderate |

The table summarizes relationship intensity across Boeing’s B2B trade flows network. We see that RTX is both a major supplier and buyer from Boeing, with Northrop Grumman and BAE Systems also securing top positions among Boeing suppliers. From a buyer’s perspective, Lockheed Martin ranks highly among Boeing corporate customers.

Specific shipment values and shipment counts underlying these relationships are available on TenderAlpha Pro. For investors, these links may be useful as a starting point for identifying counterparties that could be exposed to changes in Boeing’s production, program activity, and broader defense-industrial demand.

The TenderAlpha Pro platform also provides insights with regard to Boeing’s business with airlines across the world. The data is highly granular, presented on an individual transaction level, allowing investors to filter by harmonized system (HS) codes, which are commonly used in product classification.

As such, users can not only see trends in individual product categories, but also track individual transaction amounts for deliveries starting as little as under $1 to big-ticket purchases of almost $8 million in the case of Air India. Last but not least, this data is available for many of Boeing’s airline customers, including Turkish Airlines, which alone has 32,790 transactions with Boeing as a supplier of parts and components.

These shipment-level figures reflect trade flows records and should not be read as Boeing-recognized revenue or aircraft-delivery values.

Boeing’s Financial Performance

Now that we have seen Boeing’s government contracting activity and key B2B and commercial trade-flow relationships, let’s discuss the company’s latest financial developments.

Q1 2026 Financial Results Overview

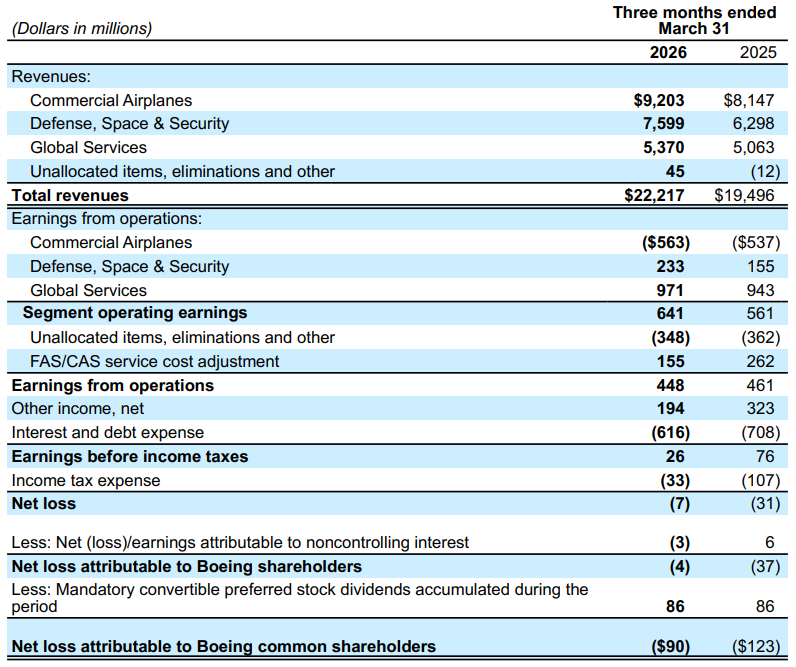

Boeing reports results in three main segments, namely Commercial Airplanes at 42% of Q1 2026 revenues, Defense, Space & Security at 34%, and Global Services accounting for the remaining 24% of Q1 2026 revenues:

Table 4: Revenue breakdown between segments

Source: Boeing quarterly report for Q1 2026

From Table 4, we can see that Boeing saw solid topline growth of 14% Y/Y, driven by broad-based strength across segments. This allowed for a comparable 14% increase in segment operating profit, buoyed by strength in Defense, Space & Security and Global Services to a smaller extent, which more than compensated for ongoing losses in Commercial Airplanes.

The bottom line result, however, remained negative, impacted by a smaller contribution from the volatile Other income component. Free cash flow was understandably negative at $1.5 billion, resulting in a net debt position of $26 billion, or around 14% of enterprise value.

As such, despite ongoing losses, Boeing’s debt position remains manageable, with the company benefiting from debt paydowns in 2025. What is more, as we will discuss in the next section, Boeing’s backlog reached new records, underpinning a more positive outlook for the rest of 2026 and into 2027.

Backlog Evolution

Boeing ended Q1 2026 with a backlog of almost $695 billion, representing a stellar 27.5% increase relative to the prior-year quarter, almost double the headline sales growth rate of 14%. All three segments contributed to the backlog increase, although Commercial Airplanes still accounts for 83% of Boeing’s total backlog, notably above the 42% contribution the segment has in Q1 2026 sales. As such, we do expect the significance of the Commercial Airplanes segment to increase once Boeing achieves higher production volumes.

Table 5: Boeing sales and backlog year-over-year evolution, 2019–2026

| Period\Indicator | Sales growth | Backlog growth |

|---|---|---|

| Q1 2026 | 14% | 27.5% |

| 2025 | 34.5% | 30.8% |

| 2024 | -14.5% | 0.2% |

| 2023 | 16.8% | 28.6% |

| 2022 | 6.9% | 7.1% |

| 2021 | 7.1% | 3.9% |

| 2020 | -24% | -21.6% |

| 2019 | -24.3% | -5.5% |

Table 5 shows that starting in 2022, backlog growth has largely exceeded topline growth, with the notable exception of 2025. As such, we believe Boeing’s medium-term revenue growth outlook is quite favorable, provided that the company can continue improving production rates and converting its record backlog into deliveries.

2026 Outlook

Looking ahead to the remainder of 2026, Boeing is expecting a near-term inflection in free cash flow generation, despite the ongoing net loss in Q1. Management continues to expect positive free cash flow of $1 billion to $3 billion for the full year, with the second half of 2026 expected to turn positive.

Table 6: Boeing 2026 Outlook

| Metric | Management commentary |

|---|---|

| 2026 free cash flow | Expected to be positive at $1 billion to $3 billion |

| Q2 2026 free cash flow | Expected to improve relative to Q1 |

| Second half of 2026 | Expected to turn positive on a free cash flow basis |

| Expected DOJ payment | Assumed to occur in the second half of the year |

| Long-term free cash flow target | $10 billion viewed as very attainable, with significant growth beyond that into the next decade |

| Key drivers beyond 2026 | Higher commercial deliveries, steady performance improvements at BDS, and continued growth at BGS |

Boeing’s medium-term free cash flow ambitions were discussed on the company’s conference call:

“Regarding our cash flow outlook, we continue to expect positive free cash flow of $1 billion to $3 billion this year, aligned with the expectations I shared last quarter. As I said previously, we benefited from order timing in the first quarter. We expect second quarter free cash flow to improve, with the second half of the year turning positive. Of note, we assume the expected DOJ payment to occur in the second half of the year.

Beyond 2026, and consistent with what we’ve discussed previously, cash flow is expected to grow, primarily driven by higher commercial deliveries, steady performance improvements at BDS, and continued growth at BGS. We continue to view the $10 billion free cash flow figure as very attainable, with significant growth beyond that into the next decade, as we execute on our record backlog and benefit from continued strong market demand.”

To sum up, the outsized increase in Boeing’s backlog in recent years underpins the company’s ambitious long-term free cash flow targets. That said, Q1 2026 results point to ongoing margin pressure, thus making future margin developments a key point of attention as topline growth appears safe.

Conclusion

Boeing relies on government contracts for approximately 38% of its 2025 revenue, with the significance of government customers likely to diminish as the company begins to work through its sizable Commercial Airplanes backlog.

Even so, government funding remains instrumental to Boeing’s operating performance, particularly during recessions and economic downturns. For instance, during the COVID-19 downturn in 2020, some 51% of Boeing’s topline was derived from government contracts. As such, we can view Boeing’s government business as a hedge to its core commercial business.

Data from TenderAlpha Pro highlights the complex ecosystem between Boeing and other aerospace & defense peers such as Lockheed Martin, Northrop Grumman, and RTX. The company’s sizable backlog and expected free cash flow inflection suggest that Boeing’s turnaround is in motion, although execution, production rates, delivery timing, and margin recovery remain the key variables to watch.

To learn more about Boeing’s G2B and B2B activity, request a demo for access to the TenderAlpha Pro platform.